Updates are announced on X (formerly Twitter) and LINE via the account "@nanahoshiuk".

Shift Nissan Tokyo (8291 JP Equity)

Presented by

This website is operated by Nanahoshi Management (UK) Ltd. (hereinafter referred to as "We").

It serves as a campaign platform targeted at shareholders of Nissan Tokyo Sales Holdings Co., Ltd. ("NTH") residing in Japan.

Recent dialogs

On 15 January 2025, we sent a letter addressed to the Representative Director and President.

Content: Follow-up on the meeting regarding cost of capital, among other matters.

Website Content

Challenges in Improving an Extremely Low PBR

Assessment of the Significantly Low Stock Price

The mechanism behind a PBR below 1x and NTH’s lack of understanding regarding the cost of capital

Concerns regarding NTH's de facto control structure and high level of treasury stock holdings

Issues related to NTH's dependence on Nissan Motor

The necessity of environmental initiatives to leverage strengths in EV sales

Issues with the Shareholder Benefit Program

The need to reconsider the purpose of the company and whether it should remain publicly listed

Challenges faced by NTH and proposed solutions

(Note: Unless otherwise stated on this website, the share price and market capitalisation are 485 yen and 32.3 billion yen, respectively, as of the closing price on March 11, 2025, and the financial data is as of the end of December 2024.

Assessment of the Significantly Low Stock Price

As shown in Annexe 1, NTH's share price is significantly discounted relative to its book value per share (BVPS), with the price-to-book ratio (hereinafter referred to as "PBR") remaining at only 0.5 times.

Furthermore, as shown in Annexe 2, NTH's PBR is at the lowest level among its industry peers.

We believe that NTH's substantial holdings of cash, cross-shareholdings, and land are undermining capital efficiency and suppressing its share price valuation. To address this issue, the company must take decisive action by divesting cross-shareholdings and monetizing surplus real estate, such as rental properties. The proceeds should be deployed either toward investments that generate returns exceeding the cost of equity or toward shareholder returns at a level at least equivalent to the cost of equity.

Annexe 1: Market Capitalization, Equity Capital, Net Cash, and Land Holdings

PBR remains at a significantly low level.

(Note: Cross-shareholding valuation accounts for expected tax deductions upon sale.)

Annexe 2: PBR Comparison Among Automotive Dealers Companies

NTH is currently valued the lowest among its listed peers.

(Note: The grey-shaded companies have already been delisted. The PBR for these companies is an estimate made by our company based on the standard share price stated in the tender offer notification that led to the delisting or the information on the date of the press release regarding the share exchange.)

Mechanism Behind a PBR Below 1x and NTH’s Lack of Understanding of the Cost of Capital

In general, as shown in Annexe 3 (yellow highlight), shareholders' value and enterprise value decrease as the cost of equity ('CoE') and the weighted average cost of capital ('WACC') increase.

In addition, as shown in Annexe 4 (green highlight), the market discounts equity capital and invested capital as ROE and ROIC are lower than CoE and WACC.

We believe that the primary reason for NTH’s low valuation is the combination of an increasing cost of capital (≈ risk and uncertainty) and declining capital efficiency. Consequently, shareholders' value can be improved by reducing the cost of capital and enhancing capital efficiency.

As per Annexe 5, NTH claims that its equity spread is positive. Theoretically, if ROE exceeds the cost of equity, PBR should be above 1x. However, NTH’s PBR remains significantly below this threshold. This suggests that the market perceives NTH’s cost of capital as higher than what the company assumes, implying that the company might be underestimating its risk.

Annexe 3: Relationship between shareholder value and cost of capital

When the cost of capital increases, shareholders' value and enterprise value decrease.

<Evaluation of shareholders' value using the dividend discount model>

<Evaluation of shareholders' value using the value driver formula>

Annexe 4: Relationship between capital efficiency and cost of capital

If capital efficiency is lower than the cost of capital, equity and invested capital are valued at a discount.

<Equity spread formula>

<EVA® (Economic Value Added) formula>

Annexe 5: Excerpt from “Measures for Achieving Management that is Conscious of Capital Costs and Stock Prices” dated November 10, 2023

The cost of equity is higher than NTH had assumed.

(Source: “Measures for Achieving Management that is Conscious of Capital Costs and Stock Prices”, page 2, dated November 10, 2023.)

Concerns Regarding Declining Capital Efficiency and Weakening Corporate Discipline

As shown in Annexe 6, 38% of NTH's voting rights are held by Nissan Network Holdings Co., Ltd. (hereinafter referred to as "Nissan Network"), which is 92% owned by Nissan Motor Co., Ltd. (hereinafter referred to as "Nissan Motor"). Given that a certain number of shareholders do not exercise their voting rights, if we adjust the combined voting rights of Nissan Network, cross-shareholding partners, and the employee stock ownership plan based on the voting participation rate, these shareholders effectively hold a majority of the voting rights. (*)

This structure results in an extremely strong influence of Nissan Network and stable shareholders who unconditionally endorse company proposals on NTH's corporate decision-making. As shown in Annexe 7, this creates governance issues similar to those seen in parent-subsidiary listings.

*According to NTH's securities report for the fiscal year ending March 2024, the total number of voting rights for common shares as of the record date for the Annual General Meeting (AGM) held in June 2024 was 664,134. However, based on the extraordinary report for the same AGM, the average number of voting rights actually exercised across all resolutions was 553,016. Therefore, dividing the exercised voting rights (553,016) by the total voting rights (664,134) results in a voting participation rate of 83.3%.

Similarly, the voting participation rate for the AGMs held in June 2023 and June 2022 was calculated at 86.1% and 87.4%, respectively. When we take the combined voting rights ratio of Nissan Network, 2 cross-shareholding partners, and the employee stock ownership plan, which amounts to 44.1% (38.11% + 2.26% + 1.9% + 1.86%), and adjust it using the range of historical voting participation rates (maximum 87.4% to minimum 83.3%), we derive a range of 50.5% to 52.3%, confirming that these shareholders effectively hold a majority of the voting rights.

As an example of the issues at hand, as shown in Annexe 8, NTH has been continuously purchasing land and buildings from Nissan Network, with the total amount reaching 7 billion yen. While it is understandable that, given the nature of the automobile sales business, acquiring real estate for strategic dealership operations may be necessary, whether such large-scale and ongoing purchases can be justified as a rational capital policy from a cost of capital perspective remains questionable.

Furthermore, as noted in the note to Annexe 6, NTH’s treasury stock has reached 10% of its total outstanding shares. If this treasury stock were to be used as consideration for acquisitions at the current low share price valuation, it would pose a serious dilution risk, further exerting downward pressure on the share price. Therefore, the prompt cancellation of treasury stock is necessary.

There are also aspects of Nissan Tokyo HD's capital policy that should be evaluated. Generally, share buybacks conducted at low share price levels are said to have a positive impact on share prices. In this regard, the share buyback announced simultaneously with the Secondary Public Offering (SPO) by the three non-life insurance companies in December 2024 (as stated in Annexe 6) can be positively evaluated, as it was conducted at a time when the share price was at a low level. However, while the estimated SPO size at the time of the announcement was 5.1 billion yen and 12.09 million shares, the corresponding share buyback program was set at 5.0 billion yen and 7.0 million shares. Since the number of shares repurchased reached 7.0 million, the total amount spent on the buyback ended at 2.96 billion yen.

Given this, we strongly urge the company to utilise the remaining 2.0 billion yen either for an additional share buyback or for a dividend increase that delivers shareholder returns at a level at least equivalent to the cost of equity.

Annexe 6: Voting Rights Ratios of Major Shareholders Reflecting the Latest Filings

Nissan Network has emerged as the dominant shareholder.

Shareholder Name

Before SPO

After SPO

1

Nissan Network Holdings Co., Ltd.

34.02%

38.11%

2

Sompo Japan Insurance Inc.

9.98%

↓1.53%

3

Tokio Marine & Nichido Fire Insurance Co., Ltd.

6.96%

↓3.11%

4

Mitsui Sumitomo Insurance Co., Ltd.

3.93%

↓2.44%

5

BNY GCM CLIENT ACCOUNT JPRD AC ISG

2.59%

2.91%

6

Alpha Co., Ltd. (Cross-shareholding partner)

2.01%

2.26%

7

Taiyo Shokai Co., Ltd.

1.76%

1.97%

8

The Master Trust Bank of Japan, Ltd.

1.74%

1.95%

9

Chuo Jidosha Kogyo Co., Ltd. (Cross-shareholding partner)

1.69%

1.90%

10

NTH Employee Stock Ownership Association

1.66%

1.86%

(Note: The shareholder ranking is based on the descending order of shareholding as stated in the major shareholders' information as of 30 September 2024. The "Pre-SPO" voting rights ratio is calculated by dividing the number of shares held as of 30 September 2024 by the total number of issued shares, excluding treasury shares. For the "Post-SPO" shareholding of Sompo Japan Insurance Inc., Tokio Marine & Nichido Fire Insurance Co., Ltd., and Mitsui Sumitomo Insurance Co., Ltd., the calculation reflects the reduction in shareholdings following the December 2024 SPO, using the shareholding figures stated in the latest change reports. The denominator for the "Post-SPO" voting rights ratio is based on the total issued shares of NTH as of 31 December 2024, excluding treasury shares (10.8%). Additionally, the classification of "Cross-Shareholding Partners" is based on the disclosure in the securities report for the fiscal year ending March 2024.)

Annexe 7: Investor Perspective on Parent-Subsidiary Listings

NTH and Nissan Motor are effectively considered a parent-subsidiary listing.

Investors recognise that companies with a certain percentage of voting rights held by a dominant shareholder, even if the holding does not exceed 50%, can still exert significant control. As a result, concerns similar to those surrounding parent-subsidiary listings arise in terms of group management and the protection of minority shareholders (ensuring the collective interests of shareholders).

Even when voting rights are below the majority threshold, factors such as actual voting behavior at shareholder meetings and governance agreements may indicate strong control or influence over the company.

Source: Tokyo Stock Exchange, Listing Department, Investor Perspective on Parent-Subsidiary Listings, February 4, 2025, p. 21.

Annexe 8: Acquisition of Land and Buildings from Nissan Network

The total amount spent on property acquisitions has reached JPY 7 billion.

Acquisition Amount (Million JPY)

FY2018

4,150

FY2019

963

FY2020

-

FY2021

489

FY2022

-

FY2023

1,398

Total

7,000

Issues Related to NTH’s Dependence on Nissan Motor

As shown in Annexe 9, it is evident that NTH's management is heavily dependent on Nissan Motor's sales strategy and supply conditions. Furthermore, as mentioned earlier, following the Secondary Public Offering (SPO), Nissan Network—a 92% subsidiary of Nissan Motor—has emerged as the dominant major shareholder. Given this shift in shareholder composition and the increasing uncertainty surrounding Nissan Motor's business environment, the risks associated with NTH's reliance on Nissan Motor have become even more pronounced.

As shown in Annexe 10, there is an indication that NTH may consider selling vehicles from other manufacturers. While NTH already sells some Renault vehicles, expanding to other brands could serve as an effective strategy to reduce its dependency risk on Nissan Motor. However, no concrete plans have been disclosed, leaving the effectiveness of this strategy uncertain.

Annexe 9: Excerpt from the Securities Report – "Business Risks" Section

Dependence on Nissan Motor is identified as a risk in the business model.

Our group’s new car sales business operates under exclusive dealership agreements concluded between our group’s automobile sales companies and specific business partners (such as Nissan Motor Co., Ltd.). The launch cycle of new models, including announcements, releases, and model changes, is primarily dictated by these business partners. Additionally, the vehicles we sell are manufactured and supplied by these specific business partners and their suppliers.

As a result, our group’s business performance may be affected by the business strategies of these specific partners and their suppliers, as well as by disruptions in production or supply caused by disasters, misconduct, or other factors. Furthermore, in the event of a sales suspension or similar issues, our company could experience significant negative impacts.

Moreover, should a disaster, misconduct, or serious negligence on the part of these specific partners or their suppliers lead to the suspension of new vehicle sales, the repercussions could extend beyond new car sales to our used car sales and automobile maintenance businesses as well.

Source: Source: Nissan Tokyo HD 112th Annual Securities Report, page 16

Annexe 10: Representative Director and President Takebayashi’s Perspective on Dependence on Nissan Motor

Summary of Q&A from the Annual General Meeting (AGM) Held in June 2024.

-

To mitigate the risk of over-reliance on Nissan, wouldn't it be prudent to start handling vehicles from other manufacturers?

-

Currently, due to the exclusive dealership agreement with Nissan, there are no plans to sell vehicles from other manufacturers. However, the company already provides inspection and after-sales services for non-Nissan vehicles. While there are no specific plans at this stage for handling other brands, the company is considering potential business expansion, including M&A, as part of its medium-term growth strategy.

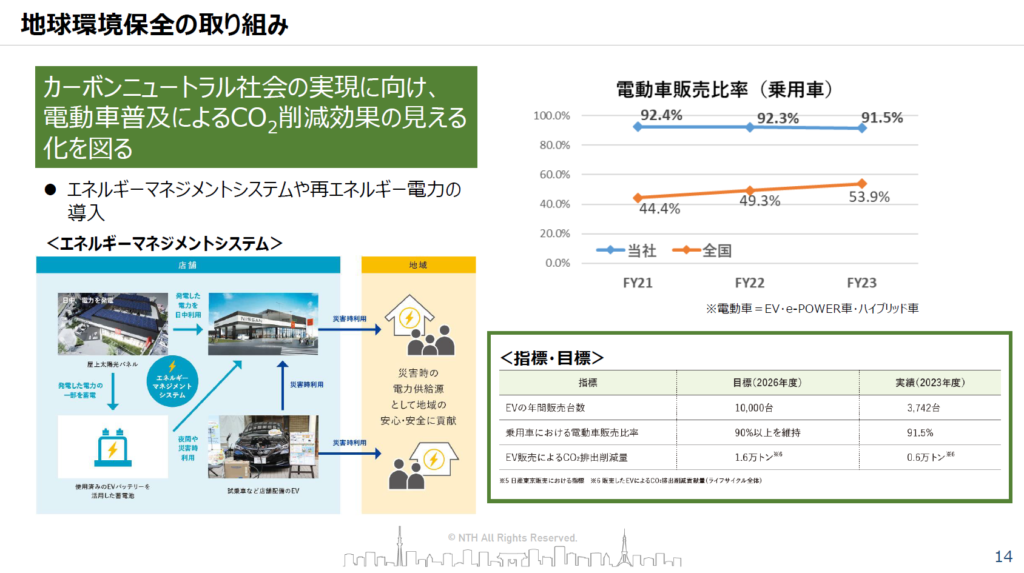

The Need for Environmental Initiatives to Leverage Strengths in EV Sales

As shown in Annexe 11, NTH has published materials from its Integrated Report, revealing that it achieved its 2026 target of a 90% electric vehicle (EV) sales ratio for passenger cars three years ahead of schedule, in 2023. Furthermore, the Integrated Report emphasizes NTH’s role as a pioneer in EV sales, stating:

"The NTH group was the first in Japan to start sales of mass production Leaf EVs in 2010. The expertise amassed in EV sales, servicing, and infrastructure over the last 14 years gives our group a tremendous advantage today. This experience solidifies the foundation for us to pursue our role as the front runner in our next stage of business."

However, as indicated in Annexe 12, the concept of "Greenwishing" has emerged. This term describes situations where companies claim to contribute to environmental sustainability, yet their actions lack meaningful impact. For example, even if a company promotes EV sales, if the electricity used to charge these vehicles is derived from coal-fired power plants, the overall reduction in greenhouse gas emissions may be negligible.

To genuinely contribute to the reduction of greenhouse gas emissions through EV sales, it is essential to decarbonize the electricity supply. If NTH aims to uphold its position as a "front-runner" in EV expansion, it must implement concrete initiatives to transition to renewable energy sources. Taking such steps will prevent EV sales efforts from being dismissed as Greenwishing and will also contribute to reducing the cost of equity.

Therefore, we believe that NTH should transparently disclose, in a quantitative manner, its initiatives for transitioning its electricity supply from fossil fuels to renewable energy within the Tokyo area, where it operates.

Annexe 11: Excerpt from the November 14, 2024, "Integrated Report Presentation Video"

NTH discloses its environmental conservation goals and achievements.

(Source: November 14, 2024, "Integrated Report Presentation Materials," )

Annexe 12: Explanation of Greenwishing

Greenwishing was first introduced in 2019 and is now included in sustainability and climate change curricula.

Greenwishing, or unintentional greenwashing, describes a practice where a company hopes to meet certain sustainability commitments but simply does not have the wherewithal to do so. Driven by the pressure to set ambitious sustainability goals, companies can find themselves committing to targets that they cannot realistically achieve, perhaps because of financial, technological or organizational constraints. Failing to achieve these targets can undermine trust in these companies and in the broader system.

Source: KPMG「Guest Post – Greenwashing, Greenhushing and Greenwishing: Don’t Fall Victim to These ESG Reporting Traps」ESG Today

Issues with the Shareholder Benefit Programme

As shown in Annexe 13, NTH provides QUO Card (a prepaid gift card widely used in Japan) as a shareholder benefit. In contrast, as indicated in Annexe 14, some industry peers offer shareholder benefits linked to their own products and services (hereinafter referred to as "company service benefits"), while others do not implement any shareholder benefit programme at all.

We understand that the primary purpose of shareholder benefit programmes is to secure stable shareholders by discouraging individual shareholders—who hold only a few trading units and primarily seek shareholder benefits—from voting against company proposals or from exercising their voting rights altogether, thereby increasing the approval rate for company-sponsored resolutions.

Another issue with shareholder benefit programmes is the disparity in effective yield when combining shareholder benefits with dividends. Since the same shareholder benefits are provided to both small-lot shareholders and those holding a significant number of shares, including institutional investors, individual investors often enjoy a relatively higher effective yield. As a result, the attractiveness of shareholder benefit programmes tends to increase, particularly among retail investors.

In particular, we view shareholder benefit programmes that rely on cash-equivalent benefits, such as QUO Cards, as problematic. These programmes increase the proportion of shareholders who prioritise receiving benefits over assessing the company’s business strategy, artificially boosting the share price. This mechanism can be considered a form of "doping" in the stock market, where share price appreciation is driven by shareholder incentives rather than the company’s fundamental value.

On the other hand, company service benefits can contribute to fostering brand loyalty and enhancing the company’s business value. By encouraging shareholders to visit company-operated stores and utilise its services, such benefits can promote purchases, increase revenue, and strengthen attachment to the brand. Therefore, shareholder benefit programmes that are expected to contribute positively to business performance should not be categorically dismissed.

In this regard, NTH’s maintenance business, which accounts for approximately one-third of its operating profit, includes vehicle maintenance, inspections, and statutory vehicle inspections, all of which are services directly relevant to individual shareholders. Given the strong compatibility between the maintenance business and company service benefits, NTH should revise its current shareholder benefit programme to leverage its own services instead.

Annexe 13: NTH's Shareholder Benefit Programme

NTH provides QUO Card as a shareholder benefit.

| Number of shares held | Shareholder special benefit (QUO Card (a prepaid gift card widely used in Japan)) | |

|---|---|---|

| Period of ownership Less than 2 years | Period of ownership 2 years or more | |

| 500 or more Less than 1,000 | 1,000 yen worth | 1,000 yen worth |

| 1,000 or more than 1,000 Less than 5,000 | 2,000 yen worth | 2,000 yen worth |

| 5,000 or more | 3,000 yen worth | 5,000 yen worth |

(Source:NTH website)

Annexe 14: Shareholder Benefit Programmes of Industry Peers

One of companies offers shareholder benefits related to its own products and services.

ICDA Holdings

- No shareholder benefit programme.

- Previously reported to have offered a Suzuka Circuit driving experience as a post-AGM benefit event.

KU Holdings

- Abolished its shareholder benefit programme (QUO Card) in 2017.

Willplus Holdings

- Abolished its shareholder benefit programme (QUO Card) in 2022.

VT Holdings

- Discount vouchers for new and used car purchases.

- Discount vouchers for vehicle inspections.

- Rental car discount vouchers.

- Discount vouchers for Keeper LABO car detailing services

Reconsidering the Purpose of the Company and Its Public Listing

The responsibility of a company's directors is to serve the shareholders who have the right to elect them by delivering returns through share price appreciation and dividends. We expect the directors of NTH to act independently of the de facto parent company, Nissan Motor, and to manage the business with a clear focus on enhancing shareholders' value.

In this regard, it is desirable for NTH to break away from its business model reliant on Nissan Motor. However, if making the strategic decision to sell vehicles from other manufacturers is deemed unfeasible, delisting should be considered as an alternative option. There is no shame in taking the company private if it is done in a way that ensures shareholders' interests are protected.

Furthermore, at the June 2024 AGM, NTH opposed a shareholder proposal calling for a dividend increase, stating that it was inconsistent with the company’s capital allocation strategy from the perspective of balancing long-term growth and shareholder returns. However, as shown in Annexe 15, the share price declined following the company’s opposition to the proposal, suggesting that market perception has worsened rather than improved.

If the management continues to neglect the abnormally low share price, it raises serious concerns about its accountability to the capital markets. If the board is unable or unwilling to pursue initiatives to enhance shareholders' value—whether through fundamental strategic changes or delisting—then it must appoint new directors who are committed to shareholders' value. In such a case, we believe the current board members should resign without delay.

Annexe 15: Total Shareholder Return (TSR) Following the Announcement of Opposition to the Shareholder Proposal in May 2024

TSR has remained weak both in absolute terms and relative to the index.

(Note: Total shareholder return is a measure of stock price performance that excludes the impact of dividends paid out. The TOPIX, when including dividends, is calculated on a post-tax basis, and similarly, NTH's dividends are recalculated and compared after taxes have been taken into account.)

Copyright © NANAHOSHI MANAGEMENT (UK) LTD. All Rights Reserved.